THE CRISIS IN PLAIN SIGHT

Cancer is the second-leading cause of death in America.

Cancer kills over 608,000 Americans every year — one person every 52 seconds.

Cancer is pervasive.

1.9 million Americans were diagnosed with cancer in 2022 — one person every 15 seconds. Nearly half of all Americans will be diagnosed with cancer at some point in their lives. Nearly 17 million Americans are living with, or have been previously treated for, some form of invasive cancer.

Cancer perpetuates racial and economic inequalities

African-Americans have the highest death rate, and shortest survival rate, of all racial and ethnic groups for most cancers. The latest research also shows that:

African-Americans experience more illness, more premature death, and worse outcomes compared to white Americans

African-American men have the highest cancer incidence of any racial or ethnic group

Cancer death rates in African-American men are twice as high as in Asians and Pacific Islanders, who have the lowest rates

Prostate cancer death rates in African-American men are more than double those of every other racial/ethnic group

African-American women are 40% more likely to die of breast cancer than white women and are twice as likely to die if they are over 50

About a third of African-American women reported experiencing racial discrimination at a health provider visit

Living in segregated communities and areas highly populated with African-Americans has been associated with increased chances of getting diagnosed with cancer after it has spread, along with having higher death rates and lower survival rates from breast and lung cancers

On average, African-Americans have just $50,000 in life insurance coverage, one-third of the $150,000 in life insurance coverage carried by white Americans. The household wealth of a typical white family in America is 8 times that of an African-American family.

These disparities make it much harder for African-Americans to survive cancer, and preserve and build household wealth after a cancer diagnosis.

Cancer inflicts catastrophic, long-lasting, and potentially lethal financial trauma

Cancer is the most expensive disease most of us will ever face.

Of the 4 Americans diagnosed with cancer every 60 seconds, 2 of them will be ruined financially.

That’s because, at an average total of $150,000, cancer treatment costs are nearly twice as high as the costs for stroke, heart attack, diabetes, epilepsy, and arthritis — combined.

While most treatment costs are covered by insurance, that doesn’t mitigate cancer’s financial damage. According to Dr. K. Robin Yabroff, “having health insurance may no longer be sufficient to protect patients and families from financial hardship” and its adverse heath outcomes.

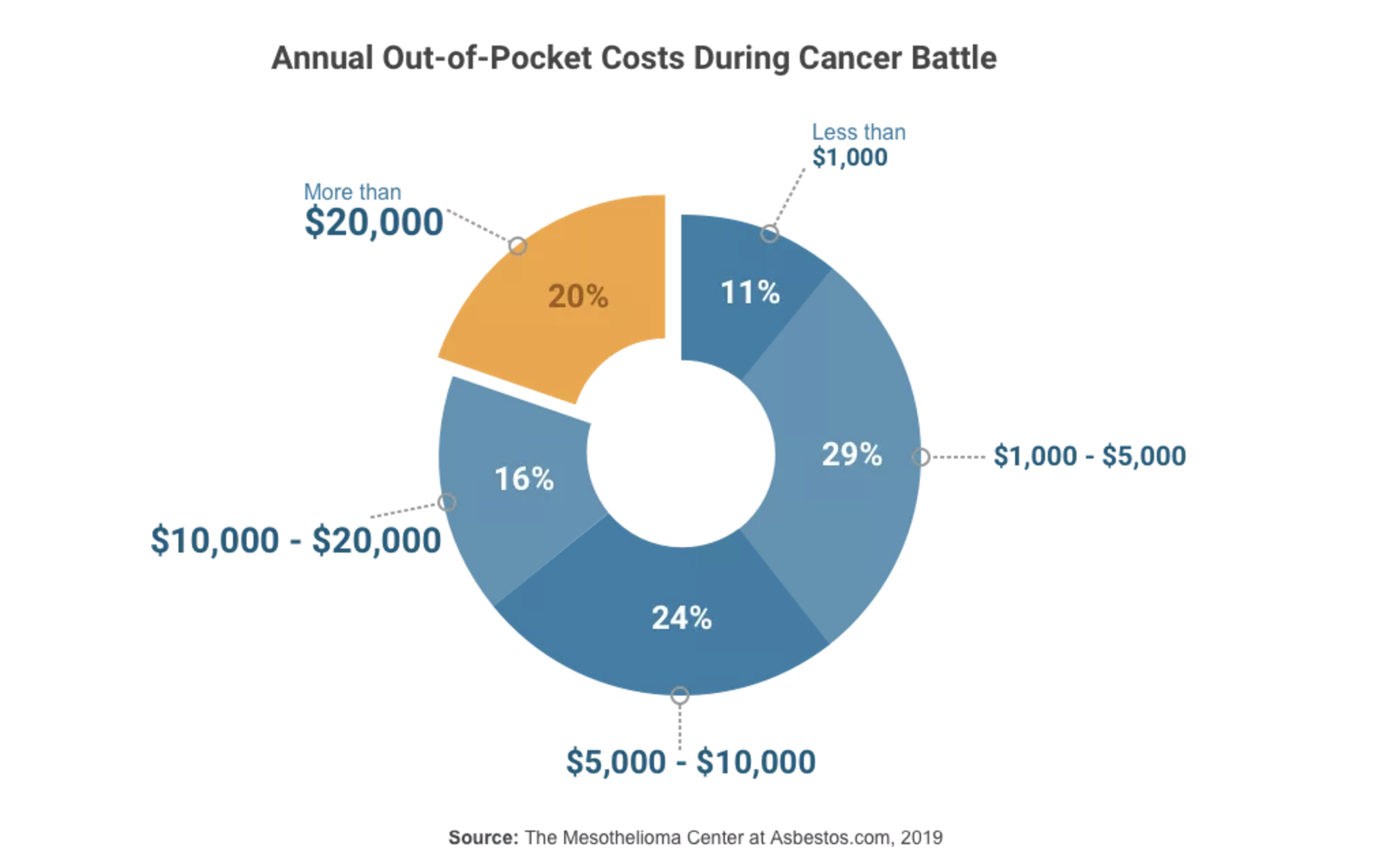

Moreover, the yearly out-of-pocket medical costs are devastating:

Up to 60% of cancer patients lose their entire life savings in the first two years of treatment. The average amount lost is over $92,000.

Between 40% to 85% of all cancer patients have to quit working during treatment, creating yet another financial burden that can last for six months or longer.

Monthly out-of-pocket costs for common cancer drugs could consume up to 70% of the average American's monthly income.

Up to 74% of adult cancer patients either delay, or skip entirely, life-saving medical procedures and prescription drug treatments due to their high cost.

They will also cut spending on, or skip entirely, other essentials like:

Gas, airfare, Uber/Lyft/taxi, and tolls to get to and from treatments

Parking, food, and lodging during treatment

Follow-up appointments with primary care physicians and specialists

Health insurance premiums and co-pays

Hospital, infusion center, surgeon, and ambulance bills

Over-the-counter medication and home health equipment

Mortgage/rent

Car payments

Groceries

Electricity, gas, water, internet, and cell phone

Child care and day care

Car insurance

Student loan payments

When they have to purchase, or get caught up on, those essentials, cancer patients often rely on installment loans, credit cards, personal loans, and revolving lines of credit.

The patient prioritizes these consumer debt payments because they assume, or have been directly told, that their financial institution has no meaningful assistance program that matches cancer’s long-term financial trauma.

If the patient falls behind on payments or runs out of available credit, interest and late charges pile up, collection efforts escalate, the patient's credit score plunges, and they no longer qualify for additional lending products.

This creates a toxic spiral of financial problems so severe that the patient sees bankruptcy as the only way out. In fact, adult cancer patients are nearly 300% more likely to file bankruptcy than those without cancer.

But that decision can be lethal, because the members who file bankruptcy have a 79% greater risk of dying early from cancer.

Credit unions aren’t doing enough.

Aside from limited efforts at a handful of institutions, credit unions — indeed, financial institutions in general — simply do not have a coherent plan to provide meaningful assistance for their members or customers with cancer that matches the overwhelming financial devastation of the disease.

Reasons include:

The false yet persistent belief that the financial catastrophe of cancer is only a healthcare or health insurance issue that doesn’t involve financial institutions

Lack of board, executive, management, and staff knowledge or curiosity about the scope and severity of this problem

Lack of demand from members because they believe their credit union can't or won't help them

Members are scared that, once they tell the credit union about their cancer-related financial trauma, the credit union will restrict access to their current credit accounts and/or refuse to consider them for other products or services

Credit union leaders balk at any institution-wide debt relief program specifically for members with cancer because they don’t want to risk allegations from state and federal regulators of disparate treatment

Financial education and counseling programs are touted as methods for hospitals, healthcare providers, and financial institutions to ease the financial toxicity of cancer.

Some studies have shown that these programs cause moderate improvement in the patient’s perceived level of financial difficulty and adherence to their treatment plan.

But post-diagnosis education and counseling programs aren’t enough. They’re akin to teaching a member about fire safety while they watch their house burn down.

Credit unions, other financial institutions, and healthcare providers regard cancer like a financial wellbeing issue to be solved by periodic education and guidance. It isn’t.

Cancer is identity theft and a house fire that traumatize the member simultaneously, a cascading series of emergencies that threaten the member’s financial, physical, and emotional health.

It requires an immediate and comprehensive response from the credit union to restore the money and security the member has lost, protect them from future losses, and pass down a positive financial legacy for their spouses, children, and dependents.

Although they’re touted as viable methods for assisting members in financial distress, credit insurance programs like life and disability coverage aren’t sufficient for the overwhelming financial distress of cancer:

Although credit life pays off the balance of the loan after the member dies, they needed that benefit while still alive because financial trauma sapped months or years from their lives

Most members will be denied for, or won’t even attempt to qualify for, disability because:

According to the Equal Employment Opportunities Commission (EEOC), cancer is not always considered a disability

It takes 3 to 5 months, at the very least, for a member to receive a decision on their disability application

Their cancer has to prevent them from working for at least 12 consecutive months to be considered disabling, a length of time that the vast majority of members can’t afford to live without income

Most disability benefits are usually 60%-70% of take-home pay, a drop in income that most members can’t afford at any time, but especially during cancer treatment

Looking back over the last 75 years, cancer is arguably the biggest and deadliest public health issue that this country has faced, a challenge made even more difficult by its unparalleled economic devastation and deep-seated racial inequities.

Financial institutions, including credit unions, have sat on the sidelines for far too long.

Your credit union can change that by joining Life Over Debt.

Life Over Debt will provide you with:

Latest research about the causes and effects of medical debt, especially debt caused by cancer

Best practices for serving your financially-distressed members that are culled from medical experts, Certified Credit Union Financial Counselors, and other credit union professionals

Procedures for crafting debt relief options specific to your member’s financial situation and loan status

Webinars and educational opportunities for your staff

Stories about your members who have been helped by debt relief and/or financial counseling, and the staff who've helped them

Resources for adapting and adopting the debt relief and financial counseling model pioneered by New Orleans Firemen’s FCU.

Life Over Debt will be supported by an intro fee and annual fee based on your asset size.

In return, you’ll help members navigate the hardest season of their lives so they can afford to heal, hope, and thrive.

References

Americans with Disabilities Act: Information for People Facing Cancer (American Cancer Society)

Cancer Disparities in the Black Community (American Cancer Society)

Cancer Facts and Figures (American Cancer Society)

Cancer Related Financial Toxicity: The National Crisis Hiding in Plain Sight (Family Reach)

Disparities in Wealth by Race and Ethnicity (US Federal Reserve)

End Terminal Debt, Pause Cancer Debt, & Essays about the Financial Struggles of Cancer Patients (Andy Janning)

In America, Cancer Patients Endure Debt on Top of Disease (Kaiser Health News)

Life Insurance Wealth Gap Statistics (Haven Life)

Side Effects: The Financial Crisis of Cancer Hiding in Plain Sight & How Credit Unions Can Help (The National Credit Union Foundation)

State Cancer Statistics (National Cancer Institute)

The Cancer Moonshot (The White House)

The High Cost of Cancer Treatment (The Mesothelioma Center)

Treating the Whole Patient with Cancer: The Critical Importance of Understanding & Addressing the Trajectory of Medical Financial Hardship (Journal of the National Cancer Institute)